HOW ARE PRICES DETERMINED IN A MARKET ECONOMY?

Prices are determined in the market through the interaction of buyers (demanders) and sellers (suppliers). In general, buyers want to buy more of the good at lower prices, less of it at higher prices; and sellers wish to sell more of the pro duct at higher prices and less of it at lower prices. How does a market deal with these opposing preferences? We need to look at these concepts of supply and demand in turn and see exactly what each entails.

DEMAND - the number of units of a good (or service) that consumers are willing (and able) to take off the market at various alternative prices, per unit of time, other things constant.

Two phrases to note:

per unit of time - denotes a flow variable; how many units that buyers will take off the market per hour, per day, per year, or whatever the specified time period.

other things constant - makes explicit the fact that there are factors other than the price of a good that influence consumer buying decisions. In order to focus on the effect of price, it is necessary to hold these other factors constant while varying the price of the good in question.

LAW OF DEMAND - there is an inverse relationship between the price of a good and the quantity demanded by consumers. In other words, holding other things constant, if we raise the price of a good, consumers will take fewer units off the market; an d if we lower the price of the good, consumers will take more of the good off the market.

In that the price of the good and the quantity demanded are inversely related, the DEMAND CURVE must slope downward to the right.

How important is price?

That question brings up the concept of ELASTICITY OF DEMAND. Elasticity is a measurement of responsiveness. Price elasticity of demand relates to the question of how sensitive consumers of a good are to changes in the price of that good. In gene ral, if c

onsumers are very responsive to a change in the price of a good, then the demand for that good would be characterized as price elastic. If on the other hand, consumers hardly respond to a change in the price of a good, we would say tha t the demand is rel

atively inelastic.

A FEW QUESTIONS TO THINK ABOUT

What determines whether the demand for a good is price elastic or inelastic? What are a few goods for which you would expect the price elasticity of demand to be very high? For what goods would you expect consumers to be relatively unresponsive to price c

hanges? Are governments more likely to place excise taxes on goods for which the demand tends to be more elastic, or less elastic? Why?

WHAT ARE THESE "OTHER THINGS" MENTIONED EARLIER?

These "other things" are factors other than the price of the product itself that determine how much of a good that consumers will buy. For example, many things we don't buy simply because we don't care for them-regardless of price. Thus we would say tha t

consumer tastes are important nonprice determinants of demand. In general, we might say that:

Qx = f(Px, T, Y, Ep, Ey, Ps, Pc, N...)

Px = price of good x

T = consumer tastes & preferences (perhaps influenced by advertising)

Y = consumer incomes (is this a positive or an inverse relationship?)

Ep = expectations concerning future prices

Ey = expectations concerning future incomes.

Ps = price of substitute goods (positive or inverse?)

Pc = price of complementary goods (sign?)

N = number of potential consumers.

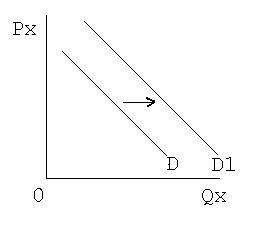

Demand versus Quantity Demanded "Demand" refers to an entire demand curve. What causes a change in demand (a shift in the demand curve)? A change in demand occurs if & only if one of the "other things" (called nonprice determinants of demand) changes. How is a change in quantity demanded shown graphically? A change in quantity demanded is shown as a movement along a given demand curve."Quantity demanded" refers to a point on a demand curve - the quantity demanded at a particular price.

How is a change in demand illustrated graphically? A change in demand is shown as a shift in the demand curve.

What causes a change in quantity demanded? A change in the price of the good brings about a change in quantity demanded. Supply - the number of units of a good that sellers will place on the market at various alternative prices, per unit of time, other things constant. Price and quantity relationship? Positive, thus the supply curve slopes upward to the right.

What are the "other things" this time? The other things which are called nonprice determinants of supply include: Pr = resource prices Tech = technology Pss = price of seller substitute goods Psc = price of seller complementary goods Ep = expectations concerning future price of the good u = other (see text) Supply versus Quantity Supplied SUPPLY = entire curve CHANGE in Supply =shift of curve WHAT CAUSES CHANGE IN SUPPLY? QUANTITY SUPPLIED - point on a curve CHANGE IN QUANTITY SUPPLIED - shown as movement along a given supply curve

What causes a change in quantity supplied? A change in the price of the good.

BE CERTAIN THAT YOU ARE ABLE TO DISTINGUISH BETWEEN THE TERMS "DEMAND" AND "QUANTITY DEMANDED"; THAT YOU ARE ABLE TO ILLUSTRATE HOW A CHANGE IN EACH IS ILLUSTRATED GRAPHICALLY; AND WHAT CAUSES A CHANGE IN EACH. ALSO, YOU MUST BE ABLE TO MAKE THE SAME DISTINCTIONS RELATIVE TO THE SUPPLY SIDE OF THE MARKET.